When starting or scaling a commercial venture, most entrepreneurs rely heavily on their personal finances. You use your own credit cards, sign personal guarantees, and risk your family’s financial security to fund your dream. But what happens when you want to land a massive contract, buy commercial real estate, or secure a low-interest six-figure loan? Your personal credit limits simply won’t cut it.

To scale safely and sustainably, you need to separate your personal and professional finances. The most effective way to do this is to build business credit.

A strong business credit profile opens doors to unsecured financing, lower insurance premiums, and premium supplier terms, all without putting your personal assets on the line. At Tradeline Distributors, we help businesses establish the solid credit foundation they need to thrive.

In this comprehensive guide, we will break down the simple steps to build business credit from scratch, maximize your scores, and unlock the commercial financing your company deserves.

Why You Need to Build Business Credit

Many small business owners assume their personal credit score is enough to carry their company. While personal credit matters, especially in the early stages, relying on it exclusively creates a bottleneck.

When you build business credit, you establish a credit asset that belongs entirely to your company. This separation offers three massive advantages:

-

Protect Your Personal Credit Score: Professional expenses are often large. If you run these expenses through personal credit cards, your credit utilization ratio skyrockets, dragging down your personal score.

-

Access Larger Funding Amounts: Financial institutions routinely grant credit limits to businesses that are 10 to 100 times higher than those offered to individual consumers.

-

Limit Personal Liability: If your business faces financial hardships, having distinct corporate credit shields your personal home, savings, and assets from commercial collections.

The Ultimate Business Credit Checklist: Building Your Foundation

Before you can actively report positive payment history, your company must exist as a legitimate, compliant, and distinct legal entity in the eyes of lenders and credit bureaus. If your business looks like a hobby on paper, banks will deny your applications automatically.

Use this foundational business credit checklist to ensure your company is structured correctly:

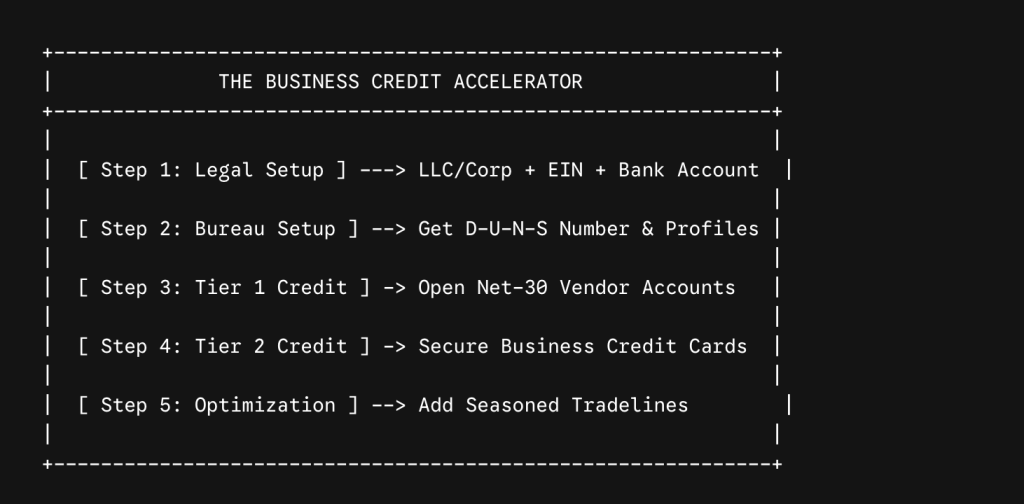

Form a Legal Business Structure

To separate yourself from your business, you cannot operate as a sole proprietorship. You must register your business as a Limited Liability Company (LLC), an S-Corporation, or a C-Corporation with your state.

Obtain a Federal Employer Identification Number (EIN)

An EIN is essentially a Social Security Number for your business. The IRS issues this number for free, and you will use it on all financial applications to track your professional credit history.

Open a Dedicated Business Bank Account

Never commingle funds. All corporate revenues and expenses must flow through a business checking account. Lenders evaluate bank statements to verify cash flow and operational legitimacy before granting business financing.

Establish a Professional Corporate Identity

Lenders utilize automated compliance software to verify your business presence. Ensure you have:

-

A physical business address (or a dedicated virtual business address; avoid standard P.O. Boxes).

-

A professional phone number listed in the National 411 Directory.

-

A company website and a professional email address matching your domain (e.g., yourname@yourbusiness.com instead of a Gmail address).

Step-by-Step Guide to Build Business Credit

Once your foundation is complete, you are ready to begin the active process to build business credit. Unlike personal credit, which accumulates automatically when you get a consumer card, corporate credit must be intentionally initiated.

Step 1: Register with the Major Corporate Credit Bureaus

Your personal credit relies on Experian, Equifax, and TransUnion. The commercial credit world, however, is governed primarily by:

-

Dun & Bradstreet (D&B): The largest commercial bureau. You must request a free 9-digit D-U-N-S Number via their website to start your file.

-

Experian Commercial

-

Equifax Business

Step 2: Open Vendor Tradelines (Tier 1 Credit)

The easiest way to jumpstart your business credit report is by opening net-30 accounts with starter vendors. These are suppliers that sell office supplies, packaging, or shipping materials and give you 30 days to pay the invoice.

The secret here is finding vendors that approve startups without a personal guarantee (PG) and actively report your payments to the bureaus. When these accounts report, they establish your earliest business tradelines.

Step 3: Maintain a Flawless Payment History

Your corporate payment performance dictates your business credit score. The most famous corporate metric is Dun & Bradstreet’s Paydex score, which ranges from 1 to 100.

-

A score of 80 is considered good and requires you to pay invoices exactly on the due date.

-

To achieve a score above 80, you must pay your bills early (often 10 to 20 days before the net terms expire).

Utilizing Credit Cards and Tradelines for Rapid Growth

As your file matures, you can move away from basic vendor accounts and scale up to more flexible financial instruments.

Leveraging a Business Credit Card

A revolving business credit card provides your business with ongoing liquidity while continuing to build your credit profile. Look for corporate cards that report exclusively to the commercial bureaus rather than consumer bureaus. This ensures that large inventory or marketing purchases won’t negatively impact your personal debt-to-income metrics.

How Premium Tradelines Accelerate the Process

Building a corporate credit score organically through net-30 vendors can take anywhere from six months to a year. For many entrepreneurs, waiting that long means missing out on immediate growth opportunities or urgent corporate funding.

This is where strategic credit optimization becomes essential. Adding established, positive credit history to your profile can significantly enhance how your company looks to lenders. By adding verified, robust history, you demonstrate to underwriters that your enterprise is capable of managing substantial financial responsibilities.

Supercharge Your Growth: Ready to take your business credit to the next level? At Tradeline Distributors, we specialize in providing the strategic financial tools necessary to optimize your commercial profile. Discover how Tradeline Distributors can help you scale today!

Understanding Your Business Credit Report and Scores

To maintain a healthy financial standing, you must understand exactly how lenders interpret your files. Unlike consumer credit reports, anyone can purchase a business credit report to review your company’s financial health, including potential partners, competitors, and clients.

Key Factors Influencing Your Business Credit Profile

While consumer scores prioritize factors like credit mix and length of history, your business credit profile focuses primarily on:

-

Payment History: Do you pay on time or early?

-

Credit Utilization: How much of your approved revolving credit lines are you using?

-

Company Size and Age: Older companies with more employees are statistically viewed as lower risk.

-

Industry Risk Classification: Your NAICS or SIC code dictates the inherent risk level of your industry (e.g., real estate or trucking is viewed differently than consulting).

Managing Your Business Credit Accounts

Regularly audit your active business credit accounts. Ensure that your vendors, suppliers, and card issuers are consistently reporting your balances and flawless payment histories. If a major trade partner does not report, ask them to submit your payment references to Dun & Bradstreet manually.

Overcoming Common Hurdles in Commercial Financing

Even if you meticulously follow the steps to build your business credit, you may encounter road blocks when applying for major loans, lines of credit, or equipment financing.

The Problem with Thin Credit Files

The most common reason for commercial loan denials is a “thin file.” This means that while your business score might technically look good, you only have one or two active lines reporting. Lenders want to see depth. They want to know that multiple organizations have extended credit to you and that you have successfully managed all of them simultaneously.

Balancing Personal and Business Risk

In the early phases of securing small business credit, lenders often require a personal guarantee. Do not be discouraged by this. As your corporate credit history grows deeper and your revenues scale, you will gain the leverage required to request true corporate financing—meaning loans backed solely by your EIN and corporate assets, completely free of personal risk.

Accelerate Your Financial Success with Tradeline Distributors

Navigating commercial credit structures can feel overwhelming, but you do not have to figure it out alone. Strategic planning and the right partnerships can compress years of trial and error into just a few weeks.

At Tradeline Distributors, we understand exactly what lenders look for when reviewing financial files. We provide the professional tools, strategic resources, and seasoned guidance necessary to build, optimize, and leverage your commercial presence. Whether you are looking to secure a new facility, expand your inventory, or establish financial independence from personal liabilities, we are here to support your mission.

Partner with Tradeline Distributors today and take control of your company’s financial future.

Frequently Asked Questions About Business Credit

How long does it take to build business credit?

With an active and organized strategy, you can establish your first initial scores (like a D&B Paydex score) within 45 to 90 days of opening and utilizing your first reporting vendor accounts. However, building a deep, robust profile capable of securing major capital typically takes 6 to 12 months.

Can I build business credit with bad personal credit?

Yes. Because business credit is tied directly to your EIN rather than your SSN, you can build a corporate profile regardless of your personal credit status. Keep in mind, however, that if a lender requires a personal guarantee for a high-limit loan, your personal credit score will be evaluated alongside your corporate file.

Do utilities and rent help my business score?

They can! If your commercial lease, internet, or utility accounts are in your exact legal business name, you can utilize commercial credit building services to self-report these monthly expenditures, adding extra positive payment depth to your profile.